You’ve built a profitable business. There’s meaningful capital sitting inside your corporation, and the strategies that worked early on are scaling less well. The embedded tax keeps growing alongside the assets.

For Canadian incorporated business owners, particularly those operating through a CCPC with substantial retained earnings, life insurance tends to come up at this point. Not as a protection product, but as a tax planning tool. This guide explains how it works, when it actually fits, and where it gets oversold.

In This Guide

Can Life Insurance Reduce Tax in Canada?

Yes, but not through deductions.

Most people expect life insurance to work like an RRSP: contribute money, get a tax break. That’s not how it works here. Premiums are generally not tax deductible. You won’t lower your taxable income by paying them.

The tax advantage comes from how the policy grows and how the money comes out. Three mechanisms drive it:

- Tax-deferred growth. Investment income inside the policy isn’t taxed annually

- Tax-free death benefit. When the policy pays out, the proceeds are generally received tax-free

- Capital Dividend Account (CDA). For corporate-owned policies, most of the proceeds can be distributed to shareholders tax-free

Each of these matters. Together, they can significantly change your after-tax outcome over a 15 to 20 year horizon. That’s why life insurance shows up in advanced planning conversations for CCPC owners, not as a product pitch, but as a structural tool for business owners who are past the basics.

You can see how this plays out in this case study on using corporate borrowing and life insurance to improve retirement income.

Why Business Owners Use Life Insurance for Tax Planning in Canada

Most incorporated owners follow the same arc. They build a profitable company, retain earnings inside the corporation, and start investing that surplus capital. Early on, that works well. A few problems compound alongside the wealth:

- Passive investment income inside a CCPC is taxed at roughly 50% combined federal and provincial, before the refundable portion is recovered through RDTOH

- Passive income over $50K starts grinding down the Small Business Deduction. At $150K, the SBD is gone, meaning a higher corporate tax rate on operating income, not just investment income

- Estate exposure grows alongside the assets, but estate planning often gets treated as a separate problem

By the time a CCPC owner has $1M to $3M in retained earnings, the question changes from “how do I grow this?” to “how do I keep more of it after tax?” That’s the shift that makes life insurance worth understanding. It’s not a product conversation. It’s a structuring conversation.

The most common question we hear: “Why hasn’t my accountant told me about this?”

Fair question. The honest answer is that accountants are focused on compliance: filing accurately, minimizing tax this year, keeping you out of trouble with CRA. Life insurance strategy sits at the intersection of tax, insurance, and estate planning. It’s nobody’s core job to bring it up proactively. Most business owners only hear about it when they ask directly, or when they work with someone whose job is to look at the full picture.

Why Traditional Tax Strategies Become Less Efficient Over Time

Salary/dividend optimization, corporate investing, RRSP contributions, and IPPs all manage tax year-to-year. They don’t address what happens as wealth compounds over decades or what happens at death.

Three structural gaps appear over time: corporate investments are taxed annually before they compound, passive income above the SBD thresholds raises the corporate tax rate on operating income, and estate planning is usually disconnected from investment strategy. At a certain point, the issue isn’t how to earn more. It’s how to lose less, both while you’re alive and when the plan eventually concludes.

How Life Insurance Reduces Tax for Business Owners in Canada

Tax-free capital flow through a corporate-owned life insurance structure.

It works through a combination of mechanisms. The value comes from how they interact over time.

Tax-Deferred Growth Inside the Policy

Permanent life insurance policies (whole life or universal life) accumulate cash value over time. Inside an “exempt” policy, which is the default structure for most Canadian permanent policies, growth on that cash value is not taxed annually.

No yearly tax on interest, dividends, or investment gains. Compounding happens without interruption.

Compare that to a taxable corporate investment account, where passive income is taxed at roughly 50% before it can compound. Over 20 years, the difference in outcomes can be substantial.

Tax-Free Death Benefit

The death benefit is generally received tax-free. If the policy is personally owned, the beneficiary receives the funds directly. If it’s corporately owned, the corporation receives the proceeds, creating a pool of tax-free capital to offset estate liabilities or facilitate wealth transfer.

Capital Dividend Account (CDA)

This is often where the most meaningful value is created, and it’s the mechanism most business owners haven’t heard of.

When a corporately owned life insurance policy pays out, the death benefit in excess of the policy’s Adjusted Cost Basis (ACB) is credited to the company’s Capital Dividend Account. A simple example:

- Death benefit: $1,000,000

- Policy ACB: $150,000

- CDA credit: $850,000

The $850,000 can be distributed to shareholders completely tax-free.

A detail most articles skip: the $150,000 that isn’t credited to the CDA still sits inside the corporation. If distributed to shareholders, it’s a taxable dividend. So “the death benefit goes to the family tax-free” is a slight oversimplification. Most of it does, but not all of it.

There’s another wrinkle that matters for timing. ACB starts high relative to the death benefit in the early years of a policy (because it includes premiums paid less the net cost of pure insurance) and grinds down over time, eventually to zero. The CDA credit gets larger the longer the policy is in force. A policy that pays out five years after issue produces a much smaller CDA credit than one that pays out thirty years in.

Practical consequence: this strategy is back-loaded. A late-life purchase doesn’t get the full CDA benefit. We’ll come back to this in “What Most Business Owners Miss.”

A common reaction here: “Why do I care about what happens when I die? I won’t be around.”

Fair. But the CDA isn’t really about you. It’s about who gets what.

The difference between $850,000 distributed tax-free and the same amount distributed as a taxable dividend isn’t abstract. It’s real money in the hands of your spouse, your kids, or whoever you’ve spent 20 years building this for. You won’t be there. They will.

See this mechanism in action in this case study on using life insurance alongside pipeline planning to preserve wealth and reduce estate tax.

Estate Liquidity Without Forced Asset Sales

At death, assets are deemed disposed and taxes are triggered. For many business owners, that creates a serious liquidity problem. Private company shares, real estate, and corporate investments aren’t easily converted to cash, but CRA’s bill is due. Without a plan, the estate may be forced to sell under pressure, accept unfavorable valuations, or distribute less than intended.

Life insurance provides immediate liquid capital to cover those obligations on your terms, not CRA’s. A business owner with $3M in corporate assets and no insurance coverage at death could face an $800K to $1.2M tax liability with no clean way to pay it. Life insurance changes that equation entirely.

Borrowing Against Policy Value

As cash value builds, the policy can be used as collateral for a third-party loan. A lender provides financing secured against the policy. You access capital without triggering a taxable disposition; the policy stays in force and compounding continues.

The most aggressive version is the Immediate Financing Arrangement (IFA), where the corp pays the premium and immediately borrows back a large portion to redeploy. The IFA is pitched as a way to capture the insurance benefits without the liquidity cost. The math can work. It also requires a cooperative lender, a policy structured for it from inception, a stable interest rate environment, and CRA tolerance for the structure (which has tightened in recent years). It’s a real strategy. It’s not a no-cost lunch.

This case study walks through a real example of using corporate borrowing backed by life insurance.

A 20-Year Example: Where the Numbers Actually Move

A simplified illustration with assumptions stated up front: 6% pre-tax annual return on both vehicles, ~50% combined corporate tax on passive investment income (RDTOH ignored for simplicity), and an “exempt” permanent policy compounding inside the policy. This is illustrative, not a projection.

A CCPC invests $50,000 a year for 20 years. In the corporate investment account, each year’s income is taxed before it compounds, so the effective compounding rate is closer to 3%. After 20 years of $50,000 deposits at roughly 3%, the account is worth approximately $1.36M.

The same $50,000 a year paid as premium into a permanent policy compounds tax-deferred. The cash value at 20 years is meaningfully higher, and at death the proceeds flow largely through the CDA to shareholders tax-free.

The exact numbers depend on policy design, fees, the cost of insurance, and other variables that an illustration from a licensed agent will spell out. The point isn’t the precise dollar figure. It’s the structural reason the gap exists: annual taxation versus tax-deferred compounding, taxable terminal disposition versus tax-free CDA flow.

This is also why the strategy doesn’t work the same way over a 5 or 10 year horizon. The math needs time.

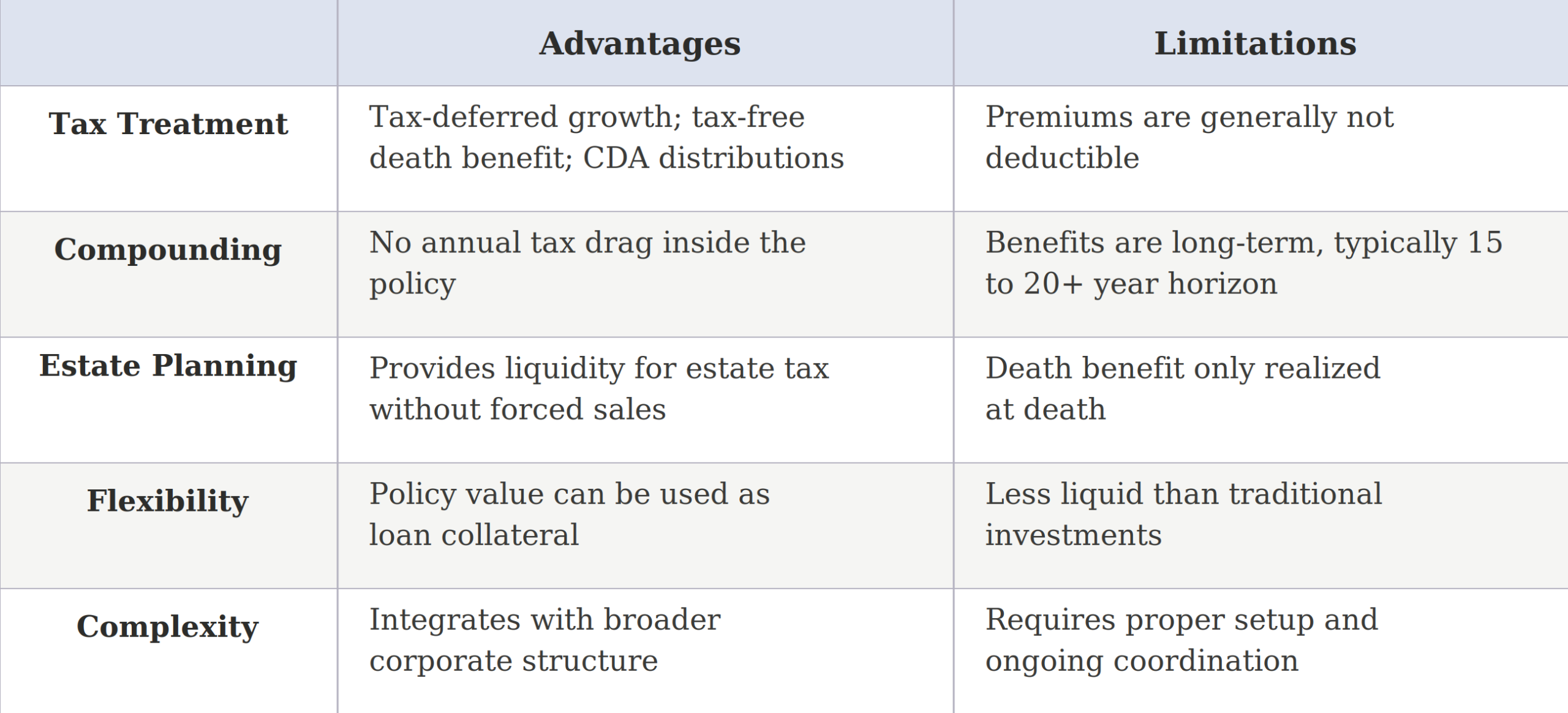

Pros and Cons of Using Life Insurance for Tax Planning

This is not a quick win. It’s a structural decision with long-term payoff, which means it needs to be evaluated as part of a broader plan, not in isolation.

Corporate-Owned vs Personally Owned Life Insurance

Ownership structure changes everything about how this strategy works.

Corporate-owned policies are typically used when retained earnings are meaningful and the goal is long-term tax efficiency. Premiums are paid with corporate dollars (generally more tax-efficient than after-tax personal funds), and the policy integrates with the CDA.

Personally owned policies are simpler, generally used for protection or straightforward estate purposes.

One thing most articles don’t mention: transferring a personally owned policy into your corporation is not a clean tax move. Subsection 148(7) of the Income Tax Act governs these transfers, and the rules were tightened in 2016 to shut down the strategy of transferring policies at fair market value to extract corporate cash tax-free. Today, the transfer is generally treated at the policy’s cash surrender value for tax purposes, which often eliminates the benefit older articles describe. If you’ve read pre-2016 content suggesting you can transfer a personal policy into the corp at FMV to pull cash out tax-free, those rules no longer apply.

Practical implication: decide on ownership structure before you buy the policy. Restructuring later is harder and more expensive than most people think.

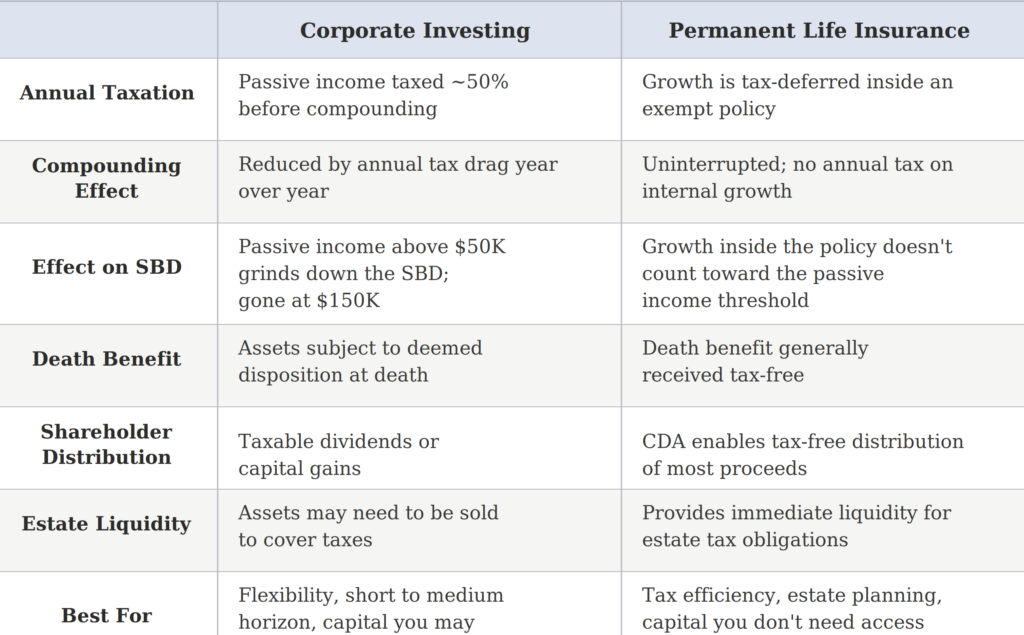

Life Insurance vs Corporate Investing in Canada

Most business owners default to investing inside their corporation. It’s familiar and flexible, but it comes with structural limitations that matter more as wealth grows.

Corporate investing isn’t wrong. It’s a core part of most plans. The question is whether it’s the right tool for every dollar of surplus capital, at every stage of wealth.

When This Strategy Makes Sense

This approach is most relevant when:

- You’re an incorporated business owner with significant retained earnings (typically $1M+)

- You have surplus capital you don’t need in the short term

- You have a long-term horizon (15 to 20+ years)

- You’re insurable (health is a meaningful gating factor)

- You’re facing meaningful estate tax exposure on shares, real estate, or RRSP/RRIF balances

- You expect to die with substantial corporate assets, not draw the corp down to zero

When It Doesn't Make Sense

- Early-stage businesses that need liquidity and flexibility

- Limited surplus capital that’s better allocated to operations or simpler strategies

- Short-term goals

- Health issues that would prevent qualification at standard rates

- An intention to spend the corporation down during retirement, rather than die with substantial assets in it

That last one is worth sitting with. If your plan is to draw the corp down through retirement to fund your lifestyle, the CDA play is worth significantly less than the brochure suggests, because there isn’t much left at death for the death benefit to amplify. Run that scenario honestly before committing to a permanent policy.

How This Fits Into a Corporate Tax Strategy

Life insurance is not a standalone solution. It works as part of a broader system: corporate structure, investment decisions, withdrawal planning, pipeline planning at death, and estate strategy. When those pieces are coordinated, outcomes improve significantly. When they’re treated separately, you leave efficiency on the table.

On its own, it’s a product. Integrated properly, it becomes a strategy that shapes how wealth is built, taxed, and transferred over a lifetime.

We’ve seen owners hold a perfectly structured corporate policy alongside a will that names the wrong beneficiary structure for their shares, and the result is a tax bill the policy was supposed to prevent. The pieces have to talk to each other.

What Most Business Owners Miss

A few things, in order of how often we see them missed:

The horizon math. Permanent insurance gets dramatically more efficient the longer the policy is in force. The CDA credit grows as ACB grinds down. Buying at 45 and dying at 85 is a very different outcome than buying at 65 and dying at 75. Most of the strategy’s value is back-loaded.

The “I’m too young to worry about this” trap. This strategy works because of time. The policy builds value over years; the longer it runs, the more efficiently it compounds. Setting this up at 45 looks very different than setting it up at 62, and by 62 you may not qualify for the same terms, or at all. The business owners who get the best outcomes structured things properly while they still had the runway to let it work.

Ownership and beneficiary mistakes. A corporately owned policy with the wrong beneficiary designation can blow up the CDA credit entirely. We’ve seen policies that should have produced a clean CDA distribution generate a taxable corporate receipt because of a checkbox that got missed at issue.

The drawdown question. If you’re going to spend the corp down to fund retirement, the CDA strategy is worth less than the brochure suggests. This is the single question that determines whether the math actually works for your situation, and it’s the one most pitches skip.

At a certain point, improving your after-tax outcome is more valuable than chasing a higher return. The business owners who recognize this early, before the retained earnings are deep and the structure is set, tend to end up in a meaningfully better position.

FAQs About Using Life Insurance for Tax Planning in Canada

Can life insurance actually reduce tax in Canada?

Yes, but not through direct deductions. The tax advantage comes from three mechanisms: tax-deferred growth inside the policy, a tax-free death benefit, and the ability to flow most corporate-owned policy proceeds through the Capital Dividend Account for tax-free shareholder distributions. The impact depends on how the policy is structured and how it integrates with your corporate plan.

Are life insurance premiums tax deductible?

In most cases, no. Personal and corporate premiums are generally not deductible. There’s a narrow exception under paragraph 20(1)(e.2) of the Income Tax Act when a policy is assigned as collateral for a business loan and certain conditions are met. These situations require careful documentation.

What is the Capital Dividend Account and how does it work?

The CDA is a notional tax account maintained by every Canadian private corporation. When a corporately owned policy pays out, the death benefit minus the policy’s ACB is credited to the CDA. The company can then elect to pay a capital dividend up to the CDA balance, received by shareholders tax-free.

Should the policy be owned by my corporation or personally?

It depends on your structure and goals. Corporate ownership makes sense when there are meaningful retained earnings, a desire to use corporate dollars efficiently, and an estate planning component. Personal ownership is simpler and works for protection-focused scenarios. Decide before you buy the policy; restructuring later is complicated by the post-2016 rules under subsection 148(7).

Can I access my policy value while I’m still alive?

Yes, two ways. First, some policies allow direct withdrawals from the cash value, though this may have tax implications. Second, the policy can be used as collateral for a third-party loan, allowing access to capital without triggering a taxable event. The second approach is more commonly used in advanced planning and requires proper structuring.

Is this strategy only for very wealthy business owners?

It’s most valuable when there’s meaningful surplus capital inside a corporation (typically $1M+ in retained earnings) and a long-term horizon. Below that threshold, simpler strategies usually offer better flexibility. Above it, the tax efficiency gains can be substantial over time.

Conclusion: From Products to Strategy

Life insurance is often sold as a protection tool. For incorporated business owners in Canada, it can be something significantly more useful: a way to improve tax efficiency over time, support how capital moves from your corporation to your family, and provide liquidity for estate tax obligations that would otherwise force difficult decisions. Individually, these are useful features. Combined, they’re a strategy.

Not every business owner needs this. But for those with meaningful retained earnings, a long-term horizon, and a growing estate tax exposure, it can materially change the outcome.

If you’ve been told to “buy a corporate policy” and the conversation didn’t include your drawdown plan, your accountant, your will, and an honest discussion of how the CDA math actually plays out over time, you weren’t getting advice. You were getting a pitch.

Have a Stone Owl advisor stress-test the structure before you commit. We’ll model the policy against your actual drawdown scenario, show you where the CDA math holds up and where it doesn’t, and tell you straight if the simpler path is the better one for your situation. Book a discovery call.